1. Outlook: Optimism Meets Reality

Finance Minister Muhammad Aurangzeb has projected a cautiously optimistic view of Pakistan’s economic trajectory, branding FY2025–26 as the year of “economic turnaround.” While the government emphasizes macroeconomic stabilization, its claims of recovery are undercut by missed growth targets, questionable data reliability, and deep-rooted structural challenges.

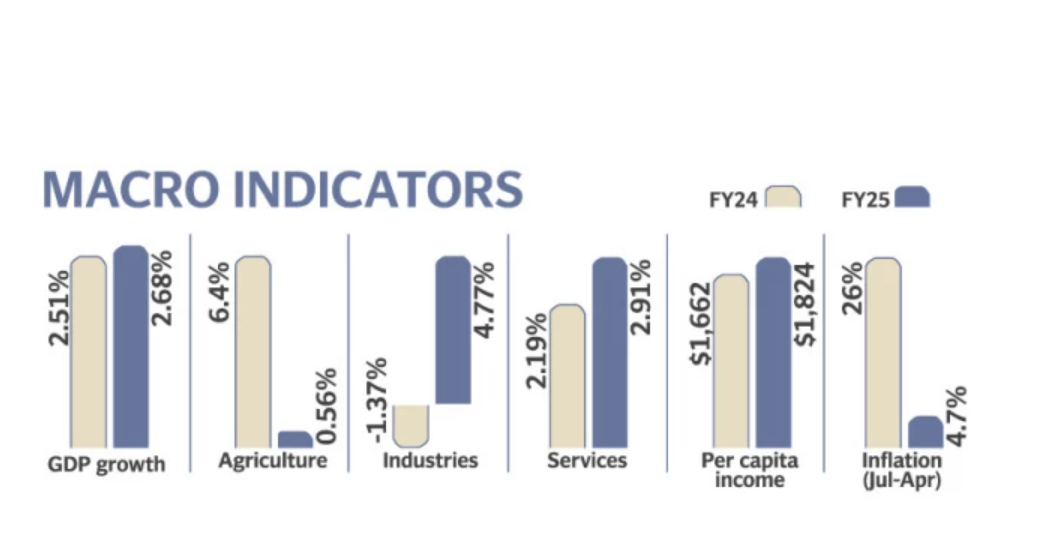

2. Growth Rate: Modest and Contested

- Claimed Growth: 2.7%

- Target: 3.6%

- Independent Assessment: Disputed

The government describes 2.7% GDP growth as sustainable and part of a longer-term trajectory to avoid past boom-bust cycles. However, economists argue this number may be overstated. If accurate, it would require a sudden, unlikely surge in economic activity in the final quarter.

Red Flags:

- A 39.3% increase in electricity sector value addition despite reported lower generation

- Sharp jumps in construction sector output amid sluggish private demand and development spending constraints

3. Inflation and Fiscal Stability: Bright Spots?

- Inflation: Down to 4.6% from over 12%

- Current Account: Expected surplus

- Foreign Exchange Reserves: $11.5 billion

The government celebrates the drop in inflation as a “fantastic story.” There is some merit to this, as inflation moderation reflects improved monetary coordination and supply-side management. However, the celebration is premature, considering:

- Underlying causes include base effects and global commodity shifts

- Real purchasing power and household consumption remain weak

On the fiscal front, Pakistan appears to have adhered to IMF guidelines, but missed tax targets by over Rs1 trillion, despite increased taxpayer registrations.

4. Investment and Private Sector: Still Lagging

- Investment-to-GDP: 13.8% (target: 14.2%)

- Private Investment: Stagnant at 9.1%

Despite initiatives under the Special Investment Facilitation Council (SIFC) to attract foreign capital, private sector confidence remains low. The lack of structural reforms—especially in contract enforcement, energy pricing, and political risk—continues to impede investment inflows.

The government’s claim that the entire public development budget of Rs1.1 trillion was utilized to stimulate growth lacks evidence and may have inflated construction and services sector numbers.

5. Agriculture: A Sector in Decline

Agriculture, long a cornerstone of Pakistan’s economy, had a disappointing year:

- Wheat: ↓ 9%

- Cotton: ↓ 31%

- Maize, rice, sugarcane: All declined

- Livestock, fishing, and forestry posted marginal gains

The narrative that agriculture could have pushed GDP growth to 3.6% had it matched last year’s output highlights its continued centrality—but also underscores persistent issues in input costs, irrigation, and policy neglect.

6. Industry and Services: Questionable Claims

Industry:

- Claimed growth: 4.77%

- Large-scale manufacturing: Negative growth of -1.53%

- Mining & quarrying: Contracted 3.4%

The industry’s growth rests on shaky ground, with electricity sector figures buoyed by subsidy accounting, and construction growth likely overstated.

Services:

- Growth: 2.91%

- Trade, transport, and finance grew modestly

- ICT showed promise with 6.5% growth, thanks to software and consultancy

While ICT growth is a bright spot, it is not yet robust enough to lift the services sector as a whole. Public administration growth, at nearly 10%, signals government expansion—not private sector dynamism.

7. Demographics and NFC Reform: A Structural Pivot

A significant policy statement came in the form of the proposed revision to the NFC award formula, suggesting:

- A move away from population-based allocations (currently 82%)

- Increased weight for poverty, area, and revenue generation

This is a bold and overdue proposal, acknowledging the need to align incentives with equity and sustainability. It could reduce the perverse incentive for unchecked population growth—though political resistance will be substantial.

8. Revenue Mobilization and Governance

- Tax base has expanded, but total revenue fell short by Rs1 trillion

- The FBR’s transformation is said to need 2–3 more years

- SOEs continue to bleed; cumulative losses hover around Rs1 trillion

Governance reforms are inching forward, but the revenue-expenditure imbalance remains Pakistan’s Achilles’ heel. Without deeper tax reforms, especially targeting untaxed sectors and leakages, fiscal consolidation will be fragile.

Conclusion: Recovery or Creative Accounting?

While the headline narrative promotes economic stabilization and cautious growth, the underlying story remains fraught with inconsistencies, fragile data assumptions, and structural weaknesses. There are some genuine improvements—like controlled inflation and growing digital remittances—but the disconnect between economic data and lived realities (poverty, unemployment, food insecurity) weakens the credibility of the official outlook.

The government is wise to frame the next year as one of consolidation and structural reform—but it will need more than optimism and statistical adjustments to deliver a real turnaround.

Verdict:

🔹 Directionally positive but statistically debatable.

🔹 Reform signals are welcome, but execution remains the true test.